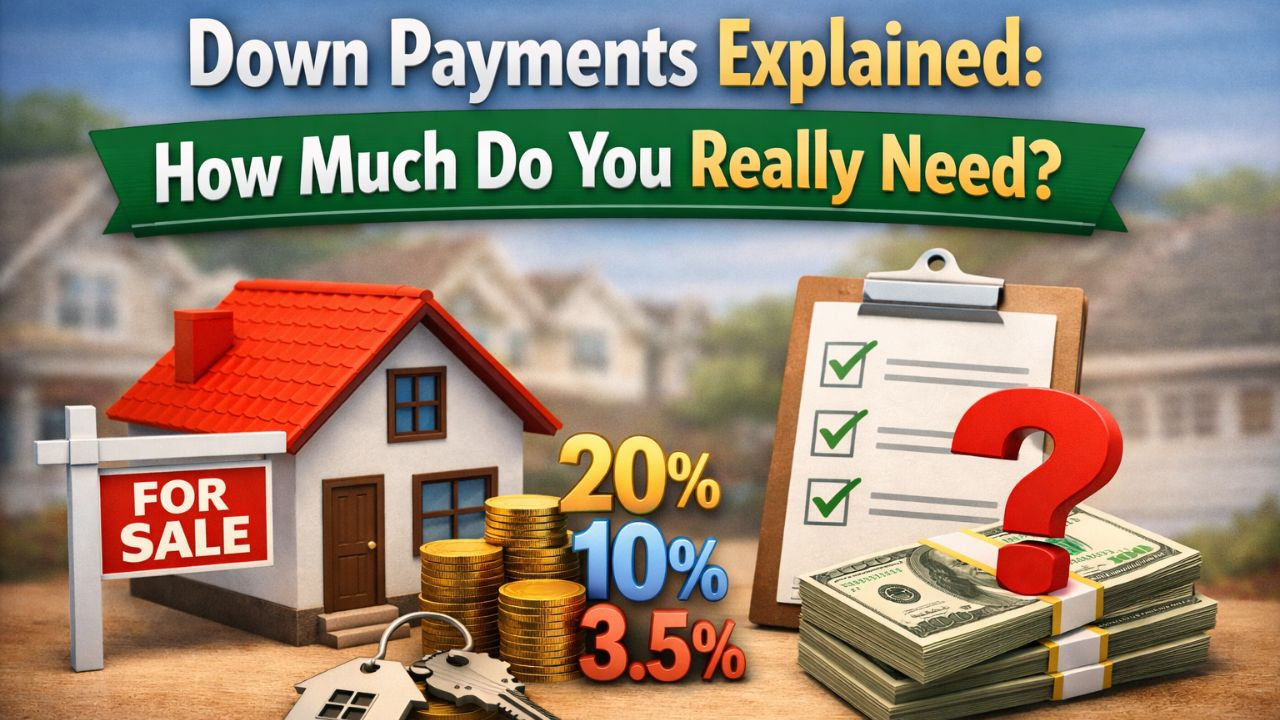

Down Payments Explained: How Much Do You Really Need?

Down Payments Explained: How Much Do You Really Need?

When it comes to buying a home, few topics cause more confusion than the down payment. Many people assume they need 20% of the purchase price saved before they can even think about applying for a mortgage—but that’s not always true. Understanding how down payments work, how they affect your loan, and what options exist can make the entire mortgage process smoother and far less intimidating.

💰 Down Payments Explaned?

A down payment is the portion of the home’s price you pay upfront. It represents your initial investment in the property and reduces the amount you need to borrow. For example, if you’re buying a $300,000 home and put down $30,000, you’re financing $270,000 through your mortgage.

This upfront payment shows lenders that you’re financially committed, which lowers their risk. In return, you often get better interest rates and lower monthly payments.

🏦 How Much Do You Really Need for a Down Payment?

The traditional rule of thumb is 20%, but that’s not a requirement for most buyers. Many loan programs allow much smaller down payments:

- Conventional loans: As low as 3% down for qualified borrowers.

- FHA loans: 3.5% down, designed for buyers with moderate credit. (Visit the FHA website Here)

- VA loans: 0% down for eligible veterans and active‑duty service members.

- USDA loans: 0% down for rural and suburban homebuyers who meet income limits.

The right amount depends on your financial situation, credit score, and long‑term goals. A larger down payment reduces your loan balance and monthly payment, but a smaller one can help you buy sooner and keep more cash available for moving costs, repairs, or savings.

📉 How Down Payments Affect Your Mortgage

Your down payment directly influences several key parts of your loan:

- Monthly Payment: The more you put down, the less you borrow—so your monthly payment decreases.

- Interest Rate: Lenders often offer lower rates to borrowers with higher down payments because they represent less risk.

- Private Mortgage Insurance (PMI): If you put down less than 20% on a conventional loan, you’ll likely pay PMI until your equity reaches that threshold. (See our article on PMI Here)

- Loan‑to‑Value Ratio (LTV): This ratio compares your loan amount to the home’s value. A lower LTV means stronger equity and better loan terms.

You can use an online mortgage calculator to test different down‑payment amounts and instantly see how they affect your monthly payment and total interest over time. It’s one of the easiest ways to visualize the trade‑offs.

🧠 Strategic Tips for Saving and Planning

If you’re still building your down payment fund, consider these strategies:

- Automate savings: Set up automatic transfers to a dedicated home‑buying account.

- Reduce high‑interest debt: Paying down credit cards improves your credit score and frees up monthly cash.

- Explore assistance programs: Many states and local governments offer grants or low‑interest loans for first‑time buyers.

- Use windfalls wisely: Tax refunds, bonuses, or gifts can accelerate your savings goal.

Even a modest increase in your down payment—say from 5% to 10%—can make a noticeable difference in your monthly costs and total interest paid.

🏡 Down Payments Explained: The Bottom Line

Your down payment is more than just a number—it’s a strategic choice that shapes your entire mortgage experience. While 20% remains a benchmark, today’s loan options make homeownership accessible with far less upfront cash. The key is understanding how your down payment interacts with interest rates, PMI, and long‑term affordability.

Before you start house hunting, use our site’s mortgage calculator to experiment with different down‑payment scenarios. Seeing the numbers side by side helps you make informed decisions and find the balance that fits your budget and goals.

Disclaimer: The information on this page is for educational purposes only and should not be considered financial or mortgage advice. Mortgage decisions depend on your personal financial situation, and you should always consult a licensed financial adviser, mortgage professional, or loan specialist before entering into any agreement.